1. April 2026

Buying an iPhone on EMI vs Saving for It, Which Is Financially Smarter?

Buying an iPhone on EMI vs Saving for It, Which Is Financially Smarter?

These days, when many of us think of buying an Iphone or any product that costs more than what we can immediately afford, the first thing we consider is buying it through EMIs.

According to reports, consumer loans through EMIs have increased significantly in India, making installment purchases more common than upfront payments. After all, it’s never been easier to opt for Easy Monthly Installments than now. With so many finance providers and no-cost EMIs available the choice feels obvious and easy to pay a decent amount every month. But is it the smarter choice compared to the old school idea of saving?

Today, at Finance Apna Apna, we’ll be discussing EMIs, budget planning, and IPhone buying tips. And, finally, how I found a different alternative that proved to be a much better option.

What is an EMI?

An EMI is formally known as an Equated Monthly Installment or Easy Monthly Installment as most people call it. It’s a specific amount that we agree to pay a lender over an agreed period of time or a financial institution to fulfill an immediate purchase, or a loan. Charging an interest is an important part of lending, as it compensates the lender for the funds that they provide and the risks associated with it.

Most important aspects of EMIs

They’re provided by lending institutions to the general population.

You must possess a healthy credit score that lending institutions check in order to evaluate your credibility. Which essentially means whether you’ll be able to pay the loan back before issuing a loan.

Institutions often provide multiple tenure options to pay back the loan through EMIs. For example: 3,6,12,24,36 months.

An interest rate is applicable which is subject to both lender and government policies.

Your monthly EMI is structured in a way that allows you to pay a part of both the principal and interest together.

Here’s how it would work with an example:

Kishor wished to buy a gaming laptop worth 50,000. He went to an e-commerce platform to buy it, and opted for EMI during the purchase. He was presented with 3 tenure options with monthly installment adjusted accordingly to complete the loan amount within that period:

3 months = ₹16,945 approx

6 months = ₹8,578 approx

12 months = ₹4,396 approx

The rate of interest applicable was 10% per annum. He chose 12 months as loan tenure. He ended up paying a total of approximately ₹55,000 for a loan amount of ₹50,000 to the lender.

To some, the interest may seem unfair but it’s an important part of lending, as it compensates the lender for the funds they provide and the risks they undertake associated with lending. But nowadays, many lenders offer no-cost EMIs.

No Cost EMIs

No cost EMIs offer you a loan to make a purchase without a yearly interest. It seems like the most ideal way yet right? It actually might be, if you don’t take the term ‘no-cost’ at face value. Because, the fact is that many times, no cost doesn’t mean, the other charges like processing fees, documentation fees, platform fees, etc are waived off. Furthermore, some discounts may no longer be applicable if you have selected No-Cost EMIs. Still, even waiving off of the interest can be quite relieving. Usually, the interest is paid by the merchant himself.

The Real Cost Of No-Cost EMIs?

None, really. Other than what we discussed above, there’s no other catch here.

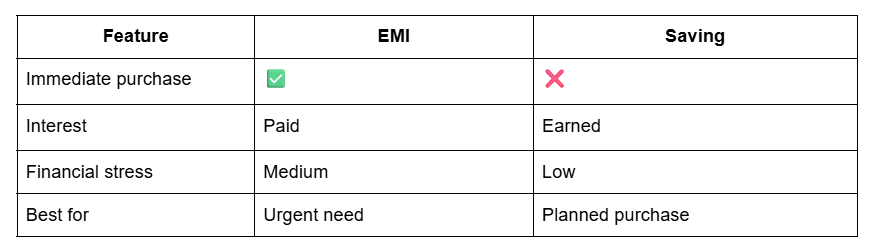

Benefits Of EMIs:

An EMI has certain benefits.

- It can be more affordable as compared to a full payment upfront.

- Fixed monthly payments relieve stress and allow better financial planning.

- It allows you to purchase and use your desired product immediately.

- Paying off EMIs on time, improves credit score and makes it easier to apply for bigger loans in the future.

Why Is Saving My Personal Favourite?

Although No-Cost EMIs offer an almost ideal way to purchase a high-ticket item without upfront paying the whole amount, and even normal EMIs significantly ease our finances by spreading payments in smaller amounts paid over multiple months, I personally found an old school way much easier and even more profitable. Here’s how I bought my new IPhone through saving.

The year was 2024, the new IPhone 16 Pro was just officially released. Everyone was hyped over the product. Just like everyone else, I couldn’t wait to get my hands on it either. As usual an EMI seemed like the most convenient option.

But, I decided to do things differently, this time.

This time, I didn’t buy the IPhone. Instead, I calculated the cost of the IPhone, divided it by 12.

IPhone 16 price in 2024: ₹1,20,000 Approx. (for the 128 GB variant).

Monthly saving calculation: ₹1,20,000/ 12 = 10,000.

I approached my local bank which I have had an account with since 6 years and opened an fixed deposit for one year. After selecting ₹1,20,000 as the total amount, I would go on to invest ₹10,000, every month into the deposit for the entire year ahead.

Fast forward to 2025:

Saving Accomplished: I had saved the entire amount of ₹1,20,000.

Earned interest instead of paying it: Received an interest of ₹7000 according to the 6.25% rates offered by my bank, instead of paying an average interest rate of 10%-20% charged by lenders.

Total amount available: ₹1,27,000.

I bought the new IPhone 17 pro without a penny of loan on me, while many were still paying their EMIs for the IPhone 16 from the previous year.

Conclusion

A healthy habit was born: The importance of saving just cannot be denied in financial planning. We have all heard about it, but most of us fail to implement it. In times like these where paying feels so much easier, savings have taken a back seat. Savings helps you collect value for future investments, dreams and goals, and build a safety net for future emergencies, ultimately making life stress free. This opportunity helped me finally build that habit.

Yet, it’s easier said than done. Because, saving a certain amount every month requires a lot of self-discipline, in contrast with a loan where it’s mandatory to pay an installment every month. But, I cannot express the joy, satisfaction, and the security that savings provide. There were some practices that made it much easier for me to build this healthy habit.

Next time, at Finance Apna Apna we’ll be discussing those things in detail, so that you, too, can easily start saving for a better future.

This article is for educational purposes only and based on personal experience and general financial principles. We prioritize integrity, ethics and your financial safety, while writing our content to keep our resources trustworthy and your finances safe. Visit our home page to know more about our vision.

FAQs

What are the best ways to buy from Apple?

While you can certainly buy an Iphone on EMI, you can pay using cash, cards, and UPI when using existing funds or savings.

Which is better EMI or full payment for mobile?

We believe making a full upfront payment is always better as it allows you to be debt-free and helps you avoid paying an 8-10% interest.

What mistake to avoid while buying phone on EMI?

Choose an EMI tenure longer than 12 months. Phones lose value fast. You’d still be paying principal and interest on the full price while the market price has become half.

Is it better to buy an iPhone on EMI?

While, buying an Iphone on EMI or any other product as such and paying installments on time can help you improve your credit score for future purchases, we recommend saving or credit. However, what’s best for you remains your personal choice.

Should I wait and buy IPhone on cash?

Yes, we’d recommend it. Two reasons, one it helps you develop a savings habit and earn interest, and second